Contents

Aiming for an MDRT membership in the UK? Let us help you get there.

A UK MDRT qualification demands a regulated, evidence-backed, repeatable business that produces enough commission, premium, or income within a calendar year.

Hitting the target, staying ethical, applying on time is crucial. But for a smooth and successful preparation, you need to understand more than that, which includes:

- what MDRT actually counts,

- which qualification route you are allowed to use,

- how UK regulation affects the path,

- how to track progress month by month, and

- how to avoid missing out because of reporting, evidence, or timing mistakes.

This guide will cover everything you need to know about qualifying for MDRT in the UK.

What is MDRT

Million Dollar Round Table (MDRT), is an international association for top-performing life insurance and financial services professionals. For UK advisers, MDRT membership is often used as a signal of strong personal production, consistent client acquisition and retention, professional credibility, and ethical conduct.

💡Good to know

MDRT is a professional achievement based on production and compliance. It is not a UK licence nor an FCA status.

MDRT is based on prior-year production

Your MDRT membership year is based on what you produced in the previous calendar year. For example, 2026 MDRT membership is based on 2025 production.

Your measurement period usually runs from 1 January to 31 December. Applications open after that production year closes. If you want to become an MDRT member in a given year, you need to treat the prior calendar year as your qualification year.

MDRT membership should be renewed annually

MDRT membership is renewed annually, meaning qualifying once does not make you a permanent annual MDRT member. You need to requalify each year under the rules for that membership year.

MDRT qualification criteria in the UK

The core MDRT requirement includes being in an eligible financial services role and meeting the annual production threshold.

When it comes to annual production threshold, MDRT allows qualification through three main methods: 1) Commission method, 2) Premium method, and 3) Income method.

Commission method is the most common route for first-time applicants in insurance-led roles. You qualify by earning enough eligible commissions paid during the production year.

With the Premium method, you qualify by generating enough eligible paid premiums. This route is helpful if your product mix is easier to track in premium terms than in commission terms.

Income method includes qualifying through eligible annual gross income from the sale of insurance and financial products. This route is important for more fee-based or planning-led advisers. However, it comes with a catch: First-time applicants generally cannot use the income method.

If you are applying for MDRT for the first time, you will typically need to qualify via commission or premium, not income, which is generally for people who have already held MDRT membership before.

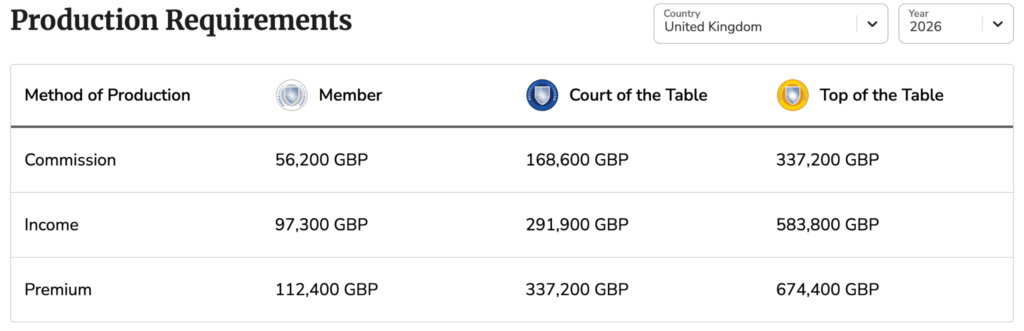

2026 MDRT UK threshold

There are three types of MDRT memberships: The MDRT (base level), Court of the table (COT), and Top of the table (TOT). The current benchmark for 2026 MDRT membership based on 2025 production are as follows:

MDRT (base level)

- Commission: £56,200

- Premium: £112,400

- Income: £97,300

Court of the Table (roughly 3x MDRT)

- Commission: about £168,600

- Premium: about £337,200

- Income: about £291,900

Top of the Table (roughly 6x MDRT)

- Commission: about £337,200

- Premium: about £674,400

- Income: about £583,800

Who qualifies for MDRT in the UK?

Usually MDRT classifies insurance and financial services products as qualifying business. For UK advisers, that can include production tied to areas such as:

- life insurance,

- critical illness,

- income protection,

- disability-related protection products (where applicable),

- certain health-related insurance categories,

- annuity and investment-related products (where MDRT rules allow credit),

- asset-based or planning fees (where eligible), and

- certain financial planning fees under the correct documentation route.

Keep in mind that not every revenue you earn necessarily counts.

What doesn’t generally count as threshold

One important thing to understand is that production is not the same as total earnings from your role. MDRT rules exclude or limit several categories. Depending on your setup, these can include the following:

- override commissions,

- manager overrides,

- training allowances,

- sign-on bonuses,

- transition packages,

- some expense allowances,

- general administrative compensation,

- non-qualifying business lines,

- revenue that is not tied to eligible product placement or advice,

In many contexts, income from general insurance or mortgage business falls outside MDRT-eligible categories. If you’re aiming for MDRT membership, consider maintaining an MDRT-only tracking sheet, rather than relying on payroll totals or broad revenue reports.

The MDRT application process in the UK

Here is what the qualifying process looks like:

Step 1: Produce enough eligible business during the calendar year

To qualify for MDRT in the UK or elsewhere, you need to meet the threshold using one method only. You cannot casually combine commission, premium, and income unless MDRT rules explicitly allow some specific treatment. Therefore, plan to qualify through a single route.

Step 2: Keep your documentation updated as you go

Do not wait until year-end. Maintain and update the following:

- insurer or platform statements,

- commission reports,

- premium reports,

- planning-fee records,

- client case logs,

- policy issue dates,

- in-force status notes,

- and internal reconciliations.

Step 3: Get your certifying letter

If you are qualifying through commission or premium, MDRT usually requires one or more certifying letters from your company or an appropriate authorised verifier. Missing or incorrect certification can delay or derail your approval.

Step 4: Apply within the application window

Applications typically open around 1 November and the standard deadline is around 1 March of the membership year, with additional fees often applying after the main deadline.

Step 5: Pay dues and complete the membership process

Complete the application, pay the fees, submit your application, and document everything properly.

Things to consider while preparing to qualify for MDRT

Many applicants aspiring to join MDRT figure out the hard part but miss the easy part. Common certifying-letter mistakes include waiting until the last minute, using the wrong signer, failing to separate product categories clearly, not reconciling paid versus expected production etc.

If you’re serious about qualifying, treat it as a year-round project. Here are more considerations:

Production is not just about sales written

MDRT generally focuses on credited business that has not been terminated by the end of the qualification period, subject to the specific rules and exceptions for that year.

If you write a lot of business that lapses quickly, gets cancelled, or never goes paid-up properly, your headline sales activity may overstate your true MDRT position. Always consider:

- selling suitable solutions,

- pre-underwriting well,

- setting client expectations properly,

- following through after issue,

- and reducing early lapses.

The term “eligible income” can sometimes be confusing

The income method sounds simple, but it can be misunderstood sometimes. Eligible income is not just your total personal earnings for the year. It is usually annual gross income derived from the sale and service of eligible insurance and financial products, subject to MDRT rules.

Here are questions you should ask:

- Was this income tied to eligible advice or product placement?

- Was it paid during the qualification year?

- Is it new business where required?

- Does part of it need to come from risk-protection activity?

- Can this income be documented in a format MDRT accepts?

If you cannot answer yes clearly, do not count it yet.

Check current rules as a first-time applicant

If you have never held MDRT membership before, do not build your plan around the income method unless you have checked the current rules carefully. This can be a big strategic mistake.

You may believe you have enough adviser income overall, but if you’re a first-time applicant and have not built enough qualifying commission or premium, you may miss the year despite having a strong business.

If this is your first MDRT attempt, structure your year around methods you are actually allowed to use.

Mistakes you’ll want to avoid:

Mistake 1: Tracking gross earnings instead of MDRT-eligible production

Mistake 2: Assuming all protection, investment, or fee income counts equally

Mistake 3: Waiting until year-end to understand the rules

Mistake 4: Relying on income method for a first-time application

Mistake 5: Ignoring placement and persistency

Mistake 6: Having weak case documentation

Mistake 7: Leaving certification until February

Mistake 8: Chasing volume instead of suitable, higher-quality cases

You are best positioned to qualify in the UK if:

- you already have a niche,

- you can generate warm introductions consistently,

- your average case size is healthy,

- your advice process is structured,

- your compliance support is good,

- and you track production accurately.

You are at higher risk of missing if:

- you depend on random lead flow,

- you do not know what counts,

- you sell broad low-margin business without a defined niche,

- you have weak post-sale follow-up,

- or your evidence and reporting are messy.

How much business do you need each month to qualify for MDRT in the UK?

From the surface, the numbers look straightforward. If your target is £56,200 in eligible commission for base MDRT, your straight-line monthly target is about £4,683 per month. But real production is never perfectly flat. Cases delay, underwriting drags, clients postpone decisions, and December can be messy.

So a better plan is:

- aim for 110% to 120% of the official target, and

- aim to be at 75% to 80% of target by the end of Q3.

That creates margin for policy delays,chargebacks, cancellations, evidence gaps, and year-end surprises.

Practical quarterly pacing example for base MDRT

- End of Q1: 20% to 25%

- End of Q2: 45% to 50%

- End of Q3: 75% to 80%

- End of Q4: 100%+ with safety margin

This strategy can be much more practical than trying to catch up on everything in December. If you want to reverse-engineer your target, break your annual MDRT number down into four business metrics:

- average eligible commission per case,

- close rate,

- number of quality appointments booked, and

- number of leads needed to generate those appointments.

Example:

Suppose your average eligible commission per placed case is £1,800. To hit £56,200, you need about 32 placed cases. If your close rate from full advice appointments to placed cases is 40%, you need about 80 quality appointments. If only 60% of booked appointments actually happen, you need roughly 133 bookings. Similarly, if 25% of warm leads convert into bookings, you need roughly 532 warm leads during the year.

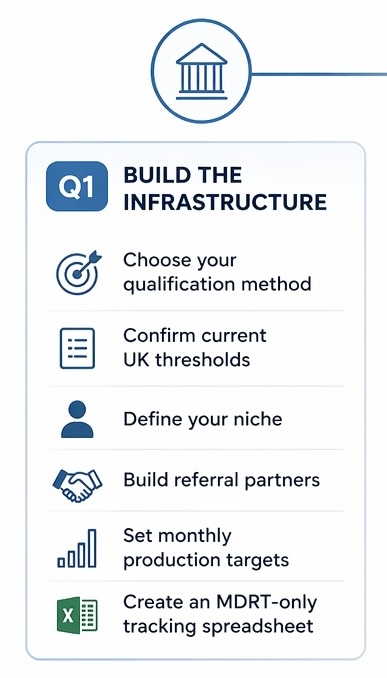

A 12-month UK MDRT game plan

Quarter 1: Build the Infrastructure

Focus on:

- choosing your qualification method,

- confirming current UK thresholds,

- defining your niche,

- building referral partners,

- setting monthly production targets,

- creating an MDRT-only tracking spreadsheet.

By the end of Q1, you should know your average case size, your top lead sources, your conversion rate, and whether you are on a commission or premium pathway.

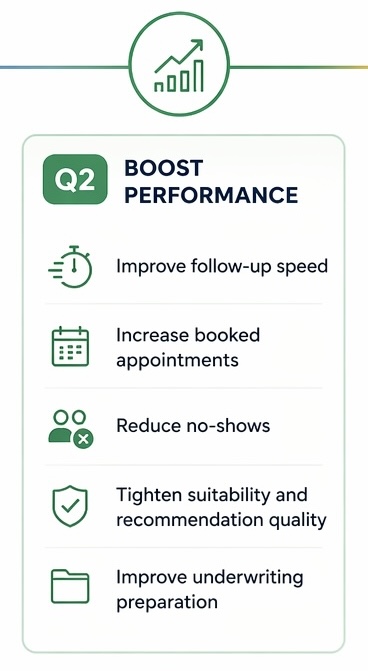

Quarter 2: Boost performance

Focus on:

- improving follow-up speed,

- increasing booked appointments,

- reducing no-shows,

- tightening suitability and recommendation quality,

- and improving underwriting preparation.

By the end of Q2, you want to be around halfway to target, or at least close enough that the gap feels achievable.

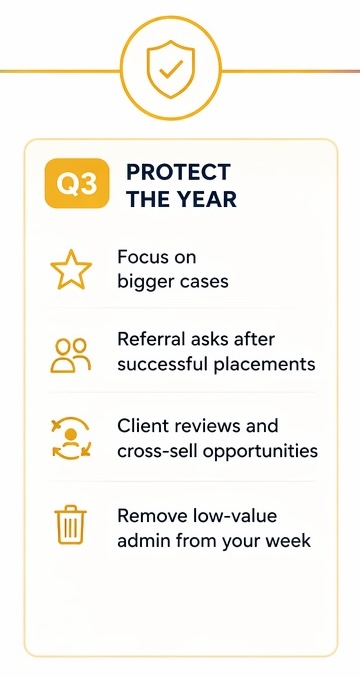

Quarter 3: Protect the year

Focus on:

- bigger cases,

- referral asks after successful placements,

- client reviews and cross-sell opportunities,

- and removing low-value admin from your week.

You should be at 75% to 80% of target or have a credible live-case pipeline to get there by the end of Q3.

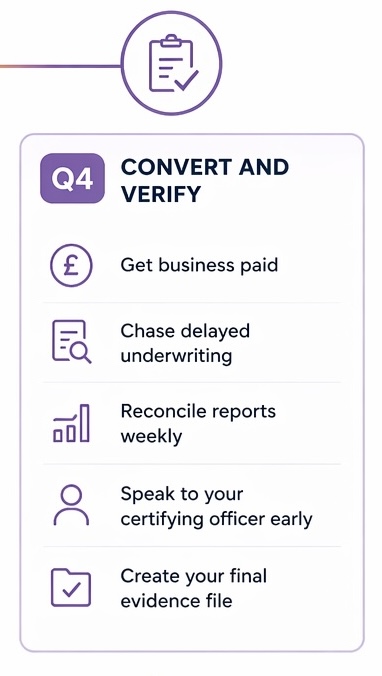

Quarter 4: Convert and verify

Focus on:

- getting business paid,

- chasing delayed underwriting,

- reconciling reports weekly,

- speaking to your certifying officer early,

- and creating your final evidence file.

By the year-end you should already know whether you qualified before the formal application opens.

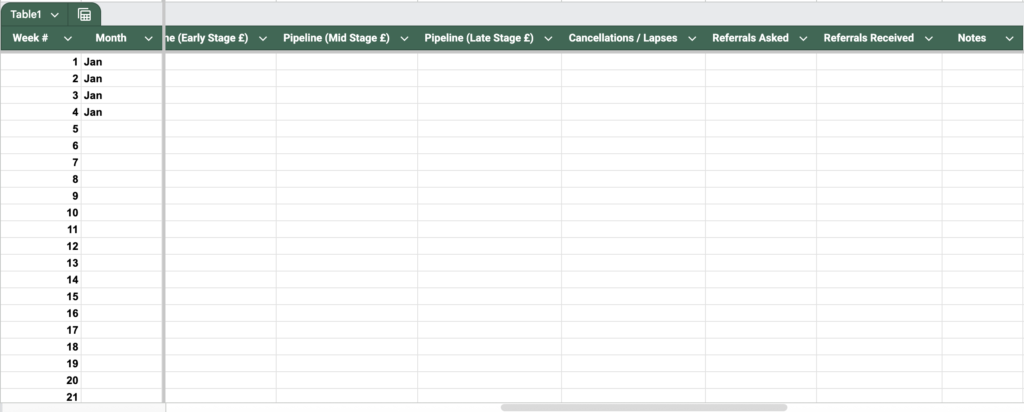

Your weekly scorecard (downloadable):

To track your MDRT steps efficiently, set up a system that allows you track your progress weekly. It’s far more useful than checking total sales once a month. Consider reviewing these numbers:

- new leads received,

- booked appointments,

- attended appointments,

- recommendations issued,

- applications submitted,

- business placed,

- eligible commission or premium credited,

- pipeline value by stage,

- cancellations or lapses,

- referrals asked for,

- referrals received.

Here’s a downloadable MDRT tracker

Download your weekly MDRT tracker here!

Final words

Meeting the MDRT production threshold may seem difficult, but it can be achieved through consistency, structure, and smart tracking. You need to generate leads consistently, manage appointments efficiently, follow up without fail, and track every piece of eligible business accurately. Trying to do all of this manually or across scattered spreadsheets is where you can lose momentum.

This is where Privyr can become a game changer.

Privyr can help you:

- track every lead and client interaction in one place,

- automate follow-ups so no opportunity slips through cracks,

- monitor your pipeline in real time, and

- measure exactly how close you are to your MDRT target.

With Privyr, you stay in control every week, instead of reacting late,

Set up your system, use your scorecard, and let Privyr do the heavy lifting behind the scenes. Try Privyr for free today!